When arranging campervan finance, common mistakes include skipping pre-approval, neglecting to check your credit score, and underestimating additional costs such as insurance and upkeep. Other pitfalls include focusing solely on monthly repayments, failing to compare multiple lenders, and choosing an excessively long loan term, which can result in owing more than the campervan’s value.

What do I wish I knew before buying a camper?

Many buyers wish they knew about hidden costs like insurance, maintenance, and campsite fees. It’s also important to understand the size and drivability that fits your lifestyle.

What to consider when buying a campervan?

Consider your budget, loan options, fuel efficiency, storage space, and the type of trips you plan to take. Check for mechanical reliability and camper features like kitchen, bathroom, and sleeping arrangements.

What not to do when buying an RV?

Don’t rush the purchase. Avoid skipping inspections, neglecting to check financing options, or buying without comparing insurance and running costs.

What are the disadvantages of a camper van?

Disadvantages include higher fuel costs, maintenance, parking challenges, and potential depreciation. Limited space can also be an issue for longer trips or families.

Purchasing a campervan or RV is an exciting step toward freedom on the open road. However, the process of securing campervan finance can feel overwhelming if you’re not prepared. From understanding loan types to evaluating interest rates, making a misstep could cost you thousands over the life of your loan. This guide will help you identify the top mistakes people make when financing a campervan and how to avoid them.

By addressing these common pitfalls, you can approach your campervan purchase confidently and ensure your investment aligns with both your lifestyle and financial goals.

1. Not Knowing Your Financing Options

One of the biggest mistakes when financing a campervan is diving in without understanding your options. Camper financing comes in different forms, including personal loans, secured vehicle loans, and specific camper trailer loans. Each option has varying interest rates, repayment terms, and eligibility requirements.

For instance, a camper trailer loan is specifically designed for trailers and often offers more flexible repayment options than a standard vehicle loan. Meanwhile, camper loans may cover motorised RVs and can include features like low-documentation options for self-employed buyers.

Failing to research these choices can lead to committing to a loan that doesn’t suit your financial situation. Take the time to compare rates, terms, and loan structures before signing any agreements.

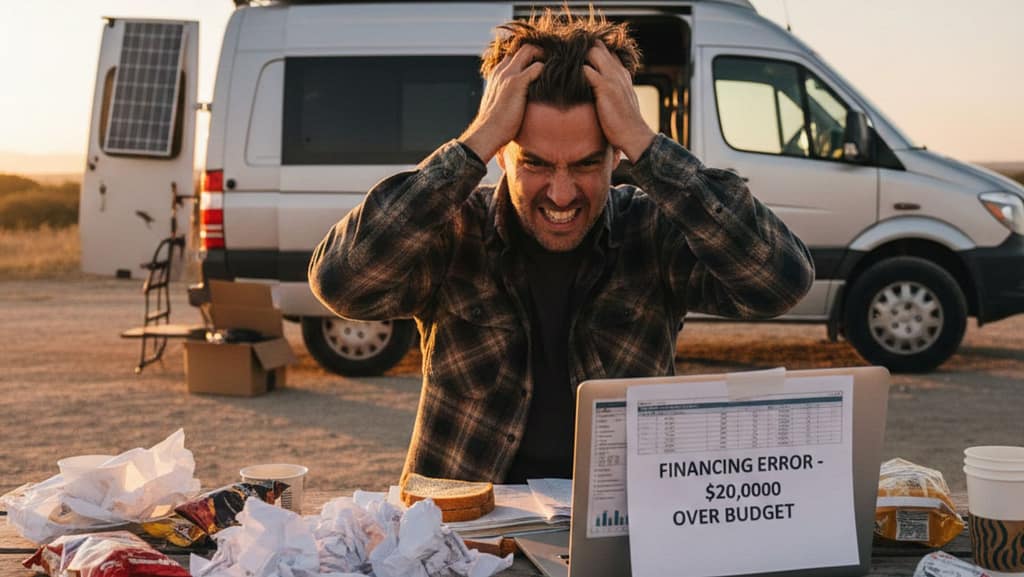

2. Overestimating What You Can Afford

It’s tempting to purchase a campervan that matches your dream adventures, but overextending financially can quickly turn a dream into a burden. Many buyers focus solely on monthly repayments without considering total costs, including insurance, maintenance, registration, and campground fees.

A common mistake is assuming pre-approval equates to affordability. While a lender may approve a certain amount, this doesn’t automatically mean it fits comfortably within your budget. Utilise a repayment calculator to determine realistic monthly obligations and avoid stretching your finances too thin.

Consider additional costs unique to campervans, such as towing equipment for a camper trailer, service plans, and fuel consumption. By planning for the full financial picture, you prevent stress and can enjoy your adventures without monetary worry.

3. Ignoring Your Credit Score

Your credit score plays a significant role in securing competitive campervan finance. A poor or limited credit history can result in higher interest rates or outright loan denial. Unfortunately, many buyers overlook this step, assuming that all camper financing options are accessible regardless of credit.

If your credit score is less than ideal, explore options like camper finance tailored for applicants with imperfect credit. These loans often have higher approval rates while still offering reasonable terms.

Checking your credit report before applying allows you to identify errors, pay down high balances, and improve your creditworthiness. The result? Lower interest rates and a smoother loan approval process.

4. Failing to Shop Around for Lenders

Many first-time campervan buyers make the mistake of settling for the first financing offer they receive. Not all lenders provide the same rates or conditions, and failing to compare can cost you thousands in interest over the life of the loan.

When exploring options, consider traditional banks, credit unions, and specialist lenders who understand the nuances of RV purchases. Specialist lenders often provide better deals for RV camper loans than standard vehicle loans.

Additionally, some lenders may offer flexible repayment schedules, deferred payments, or the option to refinance later. Don’t rush—take the time to request multiple quotes, evaluate terms, and negotiate where possible.

5. Overlooking Loan Terms and Conditions

Loan agreements can be complex, with hidden fees or restrictive conditions. Many buyers make the mistake of focusing solely on interest rates without reading the fine print.

Look out for early repayment penalties, fees for missed payments, and conditions on refinancing. Some camper financing options require comprehensive insurance coverage or restrict how the campervan can be used. For instance, certain camper loans may limit usage to personal leisure only, excluding commercial rental opportunities.

Understanding the full scope of the agreement ensures you won’t encounter unpleasant surprises after your purchase. Ask questions, clarify terms, and request documentation in writing for future reference.

6. Not Considering Residual Values and Depreciation

Campervans, like all vehicles, depreciate over time. Many buyers neglect to factor in how quickly their investment might lose value. Depreciation can affect your loan-to-value ratio, insurance premiums, and even resale value.

Financing a high-end campervan without considering depreciation could leave you owing more than the van is worth if you decide to sell early. To avoid this, research resale trends and choose a loan term that aligns with the van’s realistic depreciation rate.

This is particularly important if you are exploring luxury camper options. Specialist lenders who understand camper financing can provide guidance on managing depreciation while keeping repayments manageable.

7. Skipping Pre-Approval

Pre-approval may seem unnecessary, but it’s a powerful tool when negotiating a campervan purchase. Buyers often make the mistake of waiting until they’ve chosen a van before arranging financing.

Securing pre-approval helps you determine your budget, strengthens your position when negotiating with sellers, and speeds up the purchasing process. Many lenders offer pre-approval for camper trailer loan applications, giving you a clear understanding of your borrowing capacity.

Being prepared in advance reduces stress and prevents last-minute surprises, such as unexpected loan rejections or higher-than-expected interest rates.

8. Forgetting Insurance and Warranty Needs

Financing a campervan without considering insurance and warranties is a frequent mistake. Lenders often require comprehensive insurance to protect their investment, and failing to secure the right coverage can jeopardize your loan.

Additionally, campervans may have unique warranty requirements due to complex mechanical and electronic systems. Neglecting these aspects can lead to costly repairs down the line. Ensure your loan agreement allows for adequate insurance coverage and investigate extended warranties to protect both your investment and your journey.

Many lenders, including those offering RV camper loans, provide guidance or partner services to help you find suitable coverage options.

9. Ignoring Tax and Business Implications

For those intending to use their campervan for work purposes or rental income, understanding tax implications is crucial. Many buyers overlook how campervan expenses may impact deductions, GST obligations, or depreciation claims.

Specialist lenders often provide advice on structuring camper loans to maximize tax efficiency for self-employed or small business owners. Consulting with a financial advisor before finalizing a loan ensures you comply with regulations while optimizing benefits.

10. Not Planning for Future Upgrades or Additions

A campervan isn’t just a vehicle—it’s a mobile home. Many buyers fail to consider future upgrades, such as solar panels, satellite systems, or awnings. These additions can impact your budget and financing needs.

If you anticipate upgrading your campervan, discuss flexible loan options with your lender. Some camper financing agreements allow additional funds for improvements, helping you customize your van without taking out a second loan.

Conclusion

Financing a campervan is more than just securing a loan—it’s about planning for a lifestyle of adventure, freedom, and flexibility. By avoiding common mistakes such as underestimating costs, ignoring credit scores, or skipping pre-approval, you can secure a camper loan that aligns with your financial situation and travel dreams.

Taking the time to research your options, understand terms, and plan for insurance and upgrades ensures a smoother journey both financially and on the road. Whether you’re buying a luxury motorhome or a modest camper trailer, proper planning protects your investment and enhances your travel experience.

Curious about the best camper financing solutions available? Explore tailored options for camper loans today and find out how Alpha390 Finance can help you hit the road with confidence.